Commercial vs Non-Commercial Traders: What's the Difference?

Feb 17, 2026

The COT report divides futures market participants into three reporting categories. Each group trades for different reasons. That difference in motivation is what makes the data useful.

This post explains who each group is, why they trade, and what their positioning tells you.

The Three Groups at a Glance

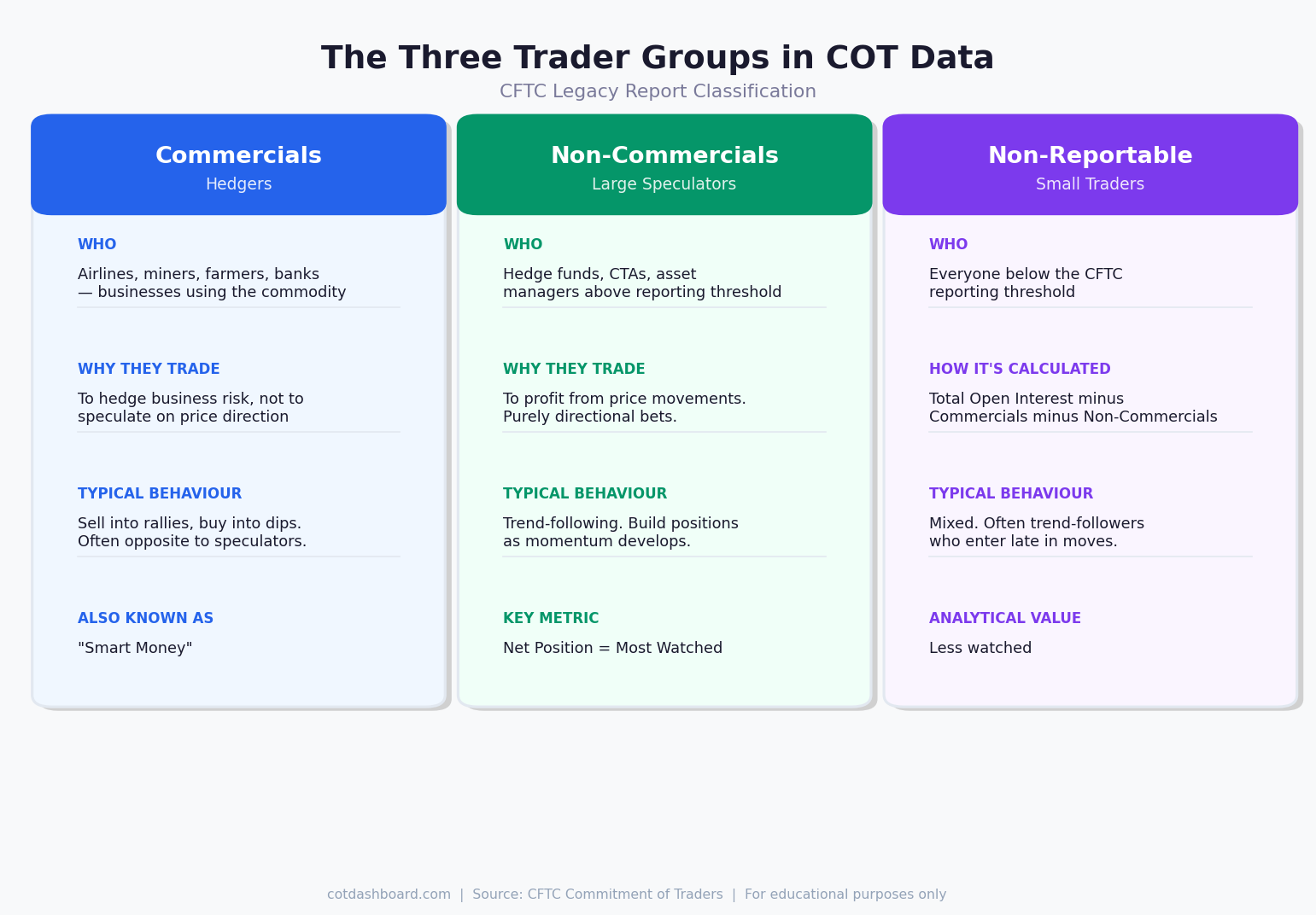

The CFTC requires large futures traders to report their positions weekly. These positions are then sorted into three categories:

- Commercials — hedgers with a business reason to hold the underlying commodity or instrument

- Non-Commercials — large speculators trading purely for profit

- Non-Reportable — everyone below the reporting threshold (mostly small retail traders)

The first two groups are where the analytical value sits. Non-reportable positions are generally treated as noise.

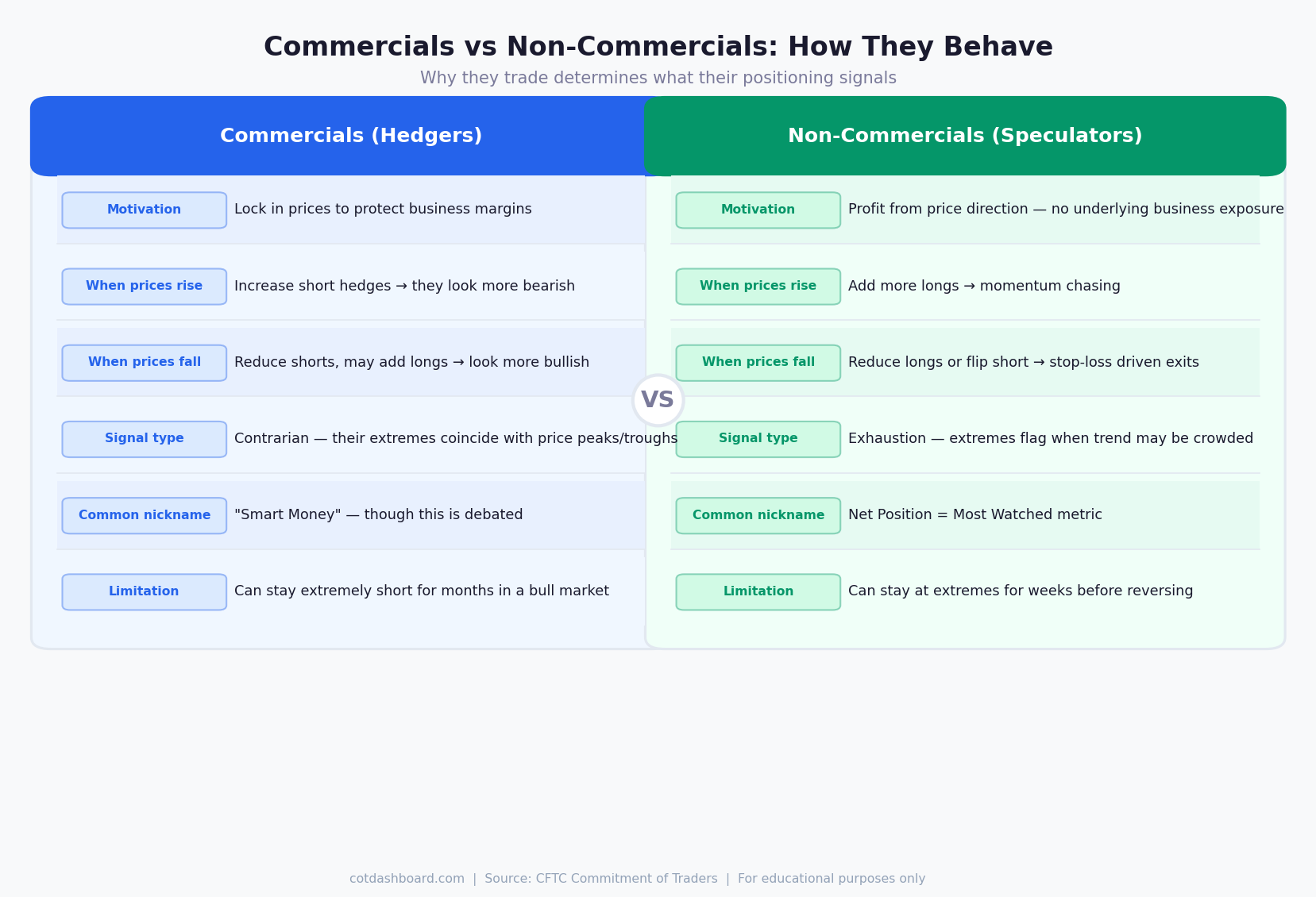

Commercials: Hedgers

Commercials are businesses that use futures to manage risk, not to speculate.

A wheat farmer shorts wheat futures to lock in a sale price before harvest. A gold mining company hedges future production. An airline buys crude oil futures to cap fuel costs. These are commercial participants — they hold the underlying asset or need it as an input.

Key characteristics:

- They are classified as commercial because they demonstrate a hedging purpose to the CFTC

- Their positions are often large and move slowly

- They frequently hold positions that are "wrong" from a short-term price perspective — and that is by design

What their positioning signals:

Commercials are often used as a contrarian indicator. When they are heavily short (i.e. heavily hedging), it usually means they expect prices to stay elevated or are locking in currently high prices. Extreme commercial short positioning in a commodity often coincides with historically high price levels.

The logic is: if a producer is aggressively locking in forward prices, they probably think current prices are attractive. That is bearish for speculative buyers.

Non-Commercials: Large Speculators

Non-commercials are funds and managed money accounts with no hedging purpose. They trade to profit from price moves.

This group includes hedge funds, commodity trading advisors (CTAs), and other large managed accounts. They take directional bets and tend to follow trends.

Key characteristics:

- Their positions reflect market sentiment and trend conviction

- They often hold large concentrated positions in one direction

- They are momentum-driven — they buy rising markets and sell falling ones

What their positioning signals:

Non-commercial positioning is the most widely followed component in COT analysis. Extreme net long or short readings are used as potential exhaustion signals.

When speculative longs are at a 5-year high, it means most of the buyers who want to own the position already own it. New buyers become scarce. The market becomes vulnerable to reversal.

This is not a precise timing tool — the signal can persist for weeks before resolving. But it identifies when a market is stretched.

Why They Move in Opposite Directions

Commercials and non-commercials frequently take opposite sides of the same trade.

When a speculator (non-commercial) goes long crude oil, someone on the other side is short. Often, that counterparty is a commercial hedger — an oil producer locking in a forward sale.

This creates a structural pattern: as speculative longs increase, commercial shorts tend to increase too. The two groups are counterbalanced by the mechanics of futures markets.

This is why COT analysis often focuses on the spread between commercial and non-commercial positioning, not just one group in isolation.

Non-Reportable: Small Traders

The non-reportable category consists of traders whose positions fall below the CFTC's reporting threshold. It is a residual — calculated by subtracting reported positions from total open interest.

This group is mostly retail traders and small funds. Their aggregate positioning rarely provides a useful signal. Some analysts treat extreme small-trader sentiment as a contra-indicator, similar to retail sentiment surveys, but the evidence is weak and inconsistent.

For practical COT analysis, focus on commercials and non-commercials.

Which Group to Watch

There is no universal answer — it depends on what you are trying to measure.

| If you want to... | Watch... |

|---|---|

| Identify potential trend exhaustion | Non-commercial extremes |

| Gauge producer conviction about prices | Commercial hedging levels |

| Measure overall speculative sentiment | Non-commercial net position |

| Spot divergences between groups | Both simultaneously |

The dashboard at cotdashboard.com tracks non-commercial positioning as the primary signal, with percentile ranks calculated over a 104-week rolling window. This lets you compare current speculative positioning to its own history — not just in absolute contract terms.

What These Categories Don't Tell You

The classification is imperfect. A large fund that also has a hedging operation can be classified as commercial. Some commodity index funds are classified as non-commercial despite being passive, not directional.

The CFTC introduced the Disaggregated COT report in 2009, which splits non-commercials into managed money, swap dealers, and other reportables. That report gives more granularity but covers fewer markets.

For most major futures markets — crude oil, gold, S&P 500, euro, Treasury bonds — the legacy COT categories remain the most widely used and most liquid dataset for positioning analysis.

For related reading, see What Is the COT Report? and What Are Percentile Rankings in COT Data?